News

Filing a return for VAT

How to submit a VAT return in UAE?

At the end of each tax period, VAT registered businesses or the ‘taxable persons’ must submit a VAT Return to the Federal Tax Authority

When are businesses required to file VAT returns?

Taxable businesses must file VAT returns with the FTA on a regular basis and usually within 28 days of the end of the ‘tax period’ as defined for each type of business. A ‘tax period’ is a specific period for which the payable tax shall be calculated and paid.

The FTA may, at its choice, assign a different tax period for certain types of businesses. Failure to file a tax return within the specified time frame will make the violator liable for fines as per the provisions of Cabinet Resolution No. 40 of 2017 on Administrative Penalties for Violations of Tax Laws in the UAE

You will need to follow the next steps to complete and file a VAT return:

Step 1 – Open the form

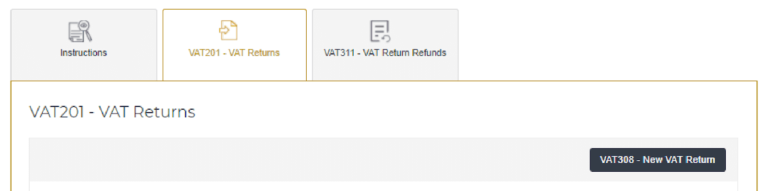

To open and access the VAT Return form, you should login to the FTA e-Services portal using your registered username and password.

To start completing your VAT Return, go to the “VAT” tab on the top bar and then go to ‘VAT201 – VAT Returns’ tab. From this screen, click on ‘VAT201 – New VAT Return’ to open the VAT Return form.

Below is an image for your reference:

Step 2 – Fill in the form as per the VAT laws and guides

When completing each box of the VAT Return form, you must:

- Insert all amounts in United Arab Emirates Dirhams (AED)

- Insert all amounts to the nearest fils (the form allows for two decimal places)

- Complete all mandatory fields

- Use “0” where necessary and where there are no amounts to be declared

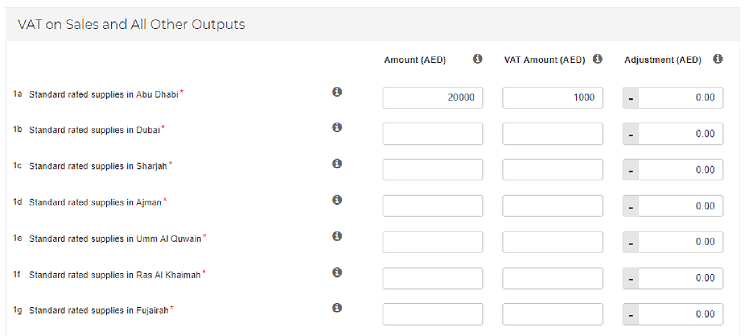

Section 1:

Below is a sample of section 1. This needs to be filed in according to each emirate. Please note that this needs to be filled in by assessing your fixed place of establishment. For businesses with fixed establishments in the UAE, the supply should be reported in the Emirate where the fixed establishment most closely connected to the supply is located. For non-established businesses, the supply should be reported in the Emirate where the supply was received.

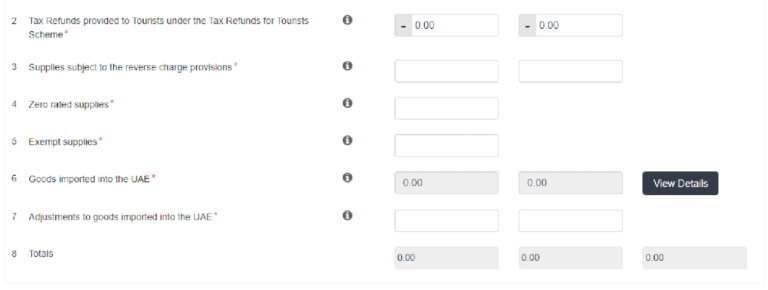

Sections 2 to 8:

Below is an extract of the sections. The following needs to be filled in as briefly explained below.

Section 2 – Tax refunds provided to tourists under the tax refunds for Tourists Scheme – These need to be filled by those retailers that are registered with Planet to refund VAT to tourists. Planet will provide them with period invoices and these need to be accounted for under this box and not as a standard rated expense (Box 9).

Section 3 – Suppliers subject to reverse charge provision – You will need to include those services that you have received from overseas vendors so that they can be subjected to VAT and reverse charges under Box 10.

Section 4 – Zero rated supplies – These are for those invoices where zero VAT has been charged. For example – Medical supplies within the UAE or export of goods and services to outside the UAE.

Section 5 – Exempt Supplies – This relates to those supplies made that are exempt from VAT. For example, life insurance, residential rents or taxis.

Section 6 – Goods imported into the UAE – This is auto-populated and the figures are taken from the customs authority automatically when you clear goods under your TRN.

Section 7 – Adjustments to goods imported into the UAE – This will only be used if you believe that there are entries under VAT box 6 that do not relate to your business or if there is any declaration missing.

Section 8 – Totals – This is the total of all the boxes from 1 to 7.

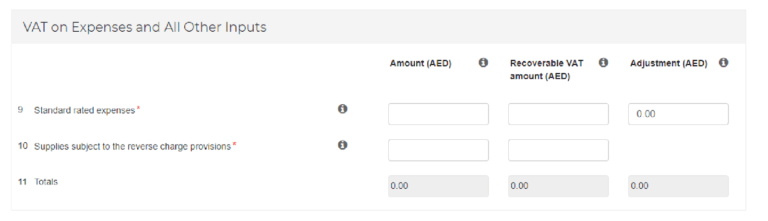

Section 9 to 11:

Below is an extract of the sections. The following needs to be filled in as briefly explained below.

Section 9 – Standard Rated Expenses – All these expenses that you have paid VAT on need to be included here (provided that they qualify for input VAT recovery).

Section 10 – Supplies subject to the reverse charge provision – This is the total of Box 3 + 6 + 7.

Once the above has been completed the value of the total output VAT and input VAT are displayed along with the total VAT liability as shown below. Box 12 , 13 and 14:

Box 15: Do you wish to request a refund for the above amount of excess recoverable tax? If you are in a net recoverable position, an option will be available on the VAT Return to request a refund of the excess recoverable tax. If ‘Yes’ is selected, you will be required to complete the VAT refund application (Form VAT311) after the VAT Return Form is submitted. If you select ‘No’, your excess recoverable tax will be carried forward to subsequent Tax Periods and can be used to offset against payable tax and/or penalties.

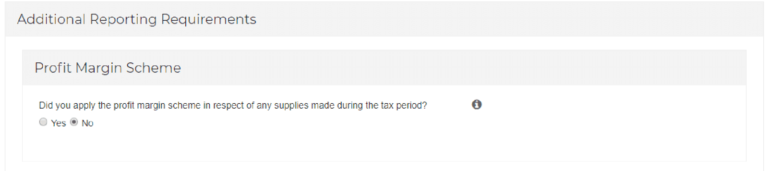

Profit Margin Scheme

You will be required to indicate whether you have used and applied the provisions of the Profit Margin Scheme during this period. Please select ‘Yes’ only if you have used the Profit Margin Scheme during the current Tax Period for which you are filing the current VAT Return.

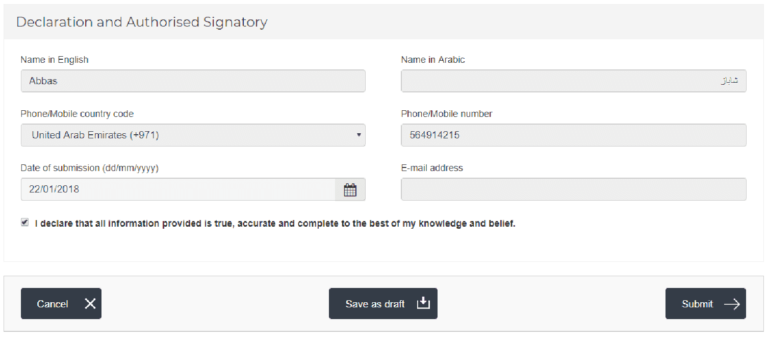

Once all has been reviewed, then the VAT from can be submitted to the Federal Tax Authority.

Making payments for VAT

The Federal Tax Authority accepts various payments methods as listed below. The registrant can use any of the following method to pay of the tax liability:

- E-Dirham card

- Debit or Credit Card

- Bank Transfer

- Deposit of cash at any exchange with you GIBAN

For further information about our services, and to find out how we can help you with taxation, get in touch with us on +971 2 671 00 33 or complete our online contact form right away!

May 7, 2020